ACC3201 Accounting Information Systems

Mar 11,22ACC3201 Accounting Information Systems

Question:

SAGA Fly Fishing, Inc.—Internal Controls Assessment

SAGA Fly Fishing, Inc., is a manufacturer of highquality flyfishing equipment that includes rods, reels, fly lines, nets, drift boats, waders, and other equipment. It also produces low-end and moderately priced spinning rods and saltwater fishing equipment, which it sells under a different brand name to protect the highquality image associated with its flyfishing division. Its home office/flyfishing production plant is located near Manchester, New Hampshire. The spinning and saltwater manufacturing plants are in upstate New York. In total, SAGA employs 1,500 workers. SAGA distributes its products worldwide through three distribution centers. Sales are currently $200 million per year and growing.

Although equipped with up-to-date production and shop floor machinery, SAGA’s Manchester plant’s inventory management, production planning, and control procedures employ little computer technology.

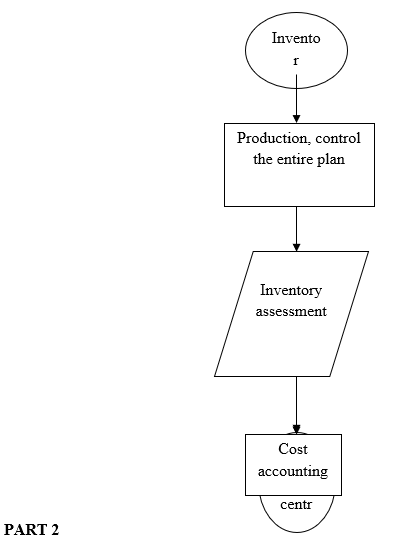

The process begins in the storekeeping department, where Mr. Holt controls the inventory and maintains the inventory records. He checks daily on the inventory control files to assess the raw material inventory needs and sends an inventory status report to production planning and control.

The production planning and control department is led by Mr. Brackenbury. Once the inventory status report is received, as well as the sales forecasts from marketing, Mr. Brackenbury takes a copy of the bill of materials and route sheet and assesses the inventory requirements. If the inventory amounts are adequate, Mr. Brackenbury prepares a production schedule, work order, move tickets, and materials requisitions, which he sends to the work centers. Mr. Brackenbury then sends a purchase requisition to the purchasing and storekeeping departments.

Mr. Brackenbury also heads the various work centers, and the supervisors of the different work centers report to him. These supervisors, upon receipt of the aforementioned documents, send the materials requisitions to the storekeeping department, and Mr. Holt sends the necessary materials to the work center. He then files a copy of the materials requisition and updates the raw material inventory ledger.

At the end of each day, he sends a copy of the materials requisitions to the cost accounting department. He also sends a journal voucher for the use of materials and a journal voucher for finished goods to the general ledger department.

In the work centers, the managers of each center collect the employees’ time cards and send them to cost accounting, along with a copy to payroll. They also send the job and move tickets, which outline the various costs that have been incurred, to cost accounting.

Ms. Kay, who heads the cost accounting department, collects all of the data, determines the overall cost, compares it to the standard costs, and determines the variances. Only the total variances are compared; the information is then used to evaluate managers and supervisors of the various departments.

Ms. Kay updates the work-in-process files and finished goods inventory files. She then creates a journal voucher and sends it to the general ledger department.

In the general ledger department, the information from the journal vouchers is entered in the general ledger computer program, where the files are updated. The journal vouchers are filed.

Required

Create a data flow diagram of the current system.

- Create a system flowchart of the existing system.

- Analyze the physical internal control weaknesses in the system. Model your response according to the six categories of physical control activities specified in the COSO internal control model.

- Prepare a system flowchart of a redesigned computerbased system that resolves the control weaknesses that you identified. Explain your solution.

Answer:

Introduction

SAGA Fly Fishing Inc.: Internal Controls Assessment

Student Name:

Student Id:

Module Name:

Abstract

In the first part of the assignment, the flowchart of the current system of the company, SAGA Fly Fishing, Inc., had been stated. In which way the system had started from inventor to cost accounting had analysed after mentioning the stages of production, planning, control, assessment and work centre. The company must have a solid internal control framework to ward off any threats on the way to productivity. Many of the faults in the internal control system of the company SAGA have been discussed here and if the flaws are neglected by the managers that can lead to further damage and loss of assets. The fundamental changes are required to be adjusted to the system. This assessment showed below provided details of the internal control model of COSO. There were mainly six kinds of tools and the name of all the tool is provided here. It has also discussed a short summary of all the internal control activities adapted by COSO. The benefits advantages associated with each of the activities and their impact on the overall management of the organisation. Each of the 6 control techniques has provided different techniques and their advantages in the current corporate world.

Table of Contents

Introduction

Introduction. 4

PART 1. 4

PART 2. 5

Conclusion. 9

References. 10

Any business operation runs smoothly facilitated by the effective internal control system. The faults in the system need to be addressed immediately and the managers must work on that to improve the work culture. It can remove all operational, administrative and technological hassles in taking valuable decisions of management.

PART 1

System flowchart

Weaknesses of physical internal control

One of the major flaws in the internal system in SAGA is that it requires technological up-gradation in production planning, control procedures and inventory management. The machinery of the shop floor is equipped with updated data yet the implementation of computer technology must be lacking therein. The areas of saltwater manufacturing and spinning plants require a little upgrading.

The inventory management system at times certainly displays efficient operational control. The sign that the same person Mr. Brackenbury is entrusted with various tasks to perform at the same time is a clear indicator of weak internal control. The separation of duties must be a solid principle to be installed into the system (Kabuye et al., 2019). The route sheet and the material bills do not maintain clarity and the assessment of inventory requirements is not perfect. The entire task of producing a schedule, preparing material requisitions is quite burdensome. On the other hand, the head of the cost accounting department is Mr. Kay, the same person who also deals with inventory files, processes files, journal vouchers and sends them to the ledger departments.

Inaccuracies occur in the reporting of inventory files, material requisitions and the accounting procedures that need to be developed. The operation does not always adhere to the industry standards and certain ethics that must be taken into consideration (Yaacoub et al., 2020). The auditors can not disclose the risks of imperfect judgement, human errors, management override and the managers tend to circumvent the control system. The inadequate discussion is held between the employers regarding protection procedures and policies.

The limitations in the efficiency of controls are increased by the pressure to carry on business with the available information. At times, the documents are found to be missing and the over domination of an employee leads to the manipulation of the files and the deception of the company. The written procedures of maintaining files and reports are not always in practice that puts forward the weakness of the system (Yaacoub et al., 2020). The absence of written procedures may create ambiguity in terms of rules and regulations. All the employees together put effort to overcome the inaccuracies in the financial statements.

The frequent customer complaints can arise out of inefficient administrative control. The price range must not vary randomly so that the customers can turn away. A proper system must be developed with a strong internal system so that consumer gratification is enhanced.

Six categories of physical control activities specified in the COSO internal control model

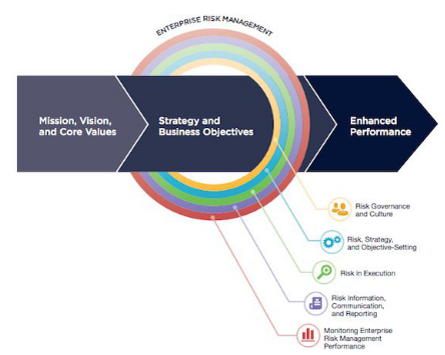

Figure 1: COSO model

Source: (Hosseinzadeh, Mehregan & Ghomi, 2019)

Risk assessment control: The internal control system of SAGA provides details of the manner in which risk must be managed and how to reduce the risks. COSO internal control models provide the management to look out the matters of internal and external potential environments (Reinisch et al., 2020). As there are many challenges in the current market, it is important for the company to overcome this uncertainty in order to future growth and success of an organisation. Many impacts are noticed in the current market scenario as there may be huge chances for new entrants. These types of situations and risks are also getting solved if the management as COSO adapts proper risk assessment activities.

Control activities: In the regulatory framework of COSO, another major important internal control model is the Control activities. Controlling is related to the overall planning process of any organisation and to checking if there are any problems. COSO has a long term vision and mission for their future but these visions will not become successful if the company fails in achieving its objectives. One of the primary aims of control activities in the internal control system is to achieve the objective of the organisation (Reinisch et al., 2020). As a part of the internal control model controlling may form part of two types Preventive and Detective. Almost all organisations like COSO have adopted this policy of controlling.

Monitoring events: An organisation mainly deals with many transactions and day to day events. COSO has employed competent individuals to monitor these events on a day to day basis. Some of the useful events in the company contained very valuable information about the company (Im et al., 2020). If these events are not reported it may lead to future difficulties. These events are related to management or finance or economical activities and are required to be quickly monitored by competent persons.

Information model: The technique for obtaining the information is based upon different conditions and situations. COSO has been able to obtain much useful information from both internal sources and external sources. Internal sources are mainly important for measuring internal control activities (Im et al., 2020). Information is delivered from top-level organisation to lower level of organisation and this information helps COSO in obtaining future requirements and expectations

Control environment: This activity in the internal control in the COSO sets many rules and standard procedures to carry out internal control activities. A proper control environment helps the organisation to reduce their mistakes and enhance their earning capacities (Hosseinzadeh, Mehregan & Ghomi, 2019). It’s also given many advantages to COSO in order to fulfil their strategic goals and visions and also to comply with all the applicable laws and compliance requirements of the company.

Communication: In order to achieve quick success and fulfilment of specified goals of the organisation as a parfait of internal control activities, the Communication system has a more vital role. This system provides that proper communication helps the efficient employees to work hard and understand their job responsibility (Hosseinzadeh, Mehregan & Ghomi, 2019). COSO has adapted all the internal control models to increase their profitability and revenue earning capacity.

Conclusion

The company strictly abide by internal procedural control to protect the assets and create reliable, accurate financial statements. The company must overcome the discussed weakness to have a sound environment where all the employees can work with confidence and loyalty. A strong culture can attract more customers with ethical appeal.

References

Hosseinzadeh, M., Mehregan, M. R., & Ghomi, M. (2019). Identifying and Analyzing Supply Chain Risks of Saipa Automobile Company using the Coso Model and Social Network Analysis (SNA). Journal of Production and Operations Management, 10(1), 111-132. DOI: DOI: https://dx.doi.org/10.22108/jpom.2018.107972.1093

Im, K., Avouac, J. P., Heimisson, E. R., & Elsworth, D. (2021). Ridgecrest aftershocks at Coso suppressed by thermal destressing. Nature, 595(7865), 70-74. DOI: https://doi.org/10.1038/s41586-021-03601-4

Kabuye, F., Kato, J., Akugizibwe, I., & Bugambiro, N. (2019). Internal control systems, working capital management and financial performance of supermarkets. Cogent Business & Management. DOI: https://doi.org/10.1080/23311975.2019.1573524

Reinisch, E. C., Ali, S. T., Cardiff, M., Kaven, J. O., & Feigl, K. L. (2020). Geodetic measurements and numerical models of deformation at Coso geothermal field, California, USA, 2004–2016. Remote Sensing, 12(2), 225. DOI: https://doi.org/10.3390/rs12020225

Yaacoub, J. P. A., Salman, O., Noura, H. N., Kaaniche, N., Chehab, A., & Malli, M. (2020). Cyber-physical systems security: Limitations, issues and future trends. Microprocessors and microsystems, 77, 103201. DOI: https://dx.doi.org/10.1016%2Fj.micpro.2020.103201